Unpacking Dual Momentum

A Smart Twist on Tactical Asset Allocation

Hey there! Today, let's dive into the intriguing world of "Dual Momentum" and see how it spices up tactical asset allocation (TAA) strategies. Ever thought about using the momentum factor to jazz up your investment strategy? Dual Momentum might just be the trick you need.

What's Dual Momentum Anyway?

Brought into the spotlight by Gary Antonacci in his 2014 book, "Dual Momentum Investing: An Innovative Approach for Higher Returns with Lower Risk," this strategy is all about playing it smart with two types of momentum: absolute and relative.

Absolute Momentum (also known as time-series momentum): This one's like taking a selfie, comparing an asset's current performance to its past self, and giving a thumbs up to those showing a positive vibe.

Relative Momentum (also known as cross-sectional momentum): Here, we're sizing up everyone in the room, picking out the ones who are out-dancing the rest.

Put them together, and you've got a strategy that's not just chasing after winners but also making sure those winners are leading the pack. It's about betting on assets that are not only doing well on their own but are also beating their peers.

Spotlight on Global Equities Momentum (GEM)

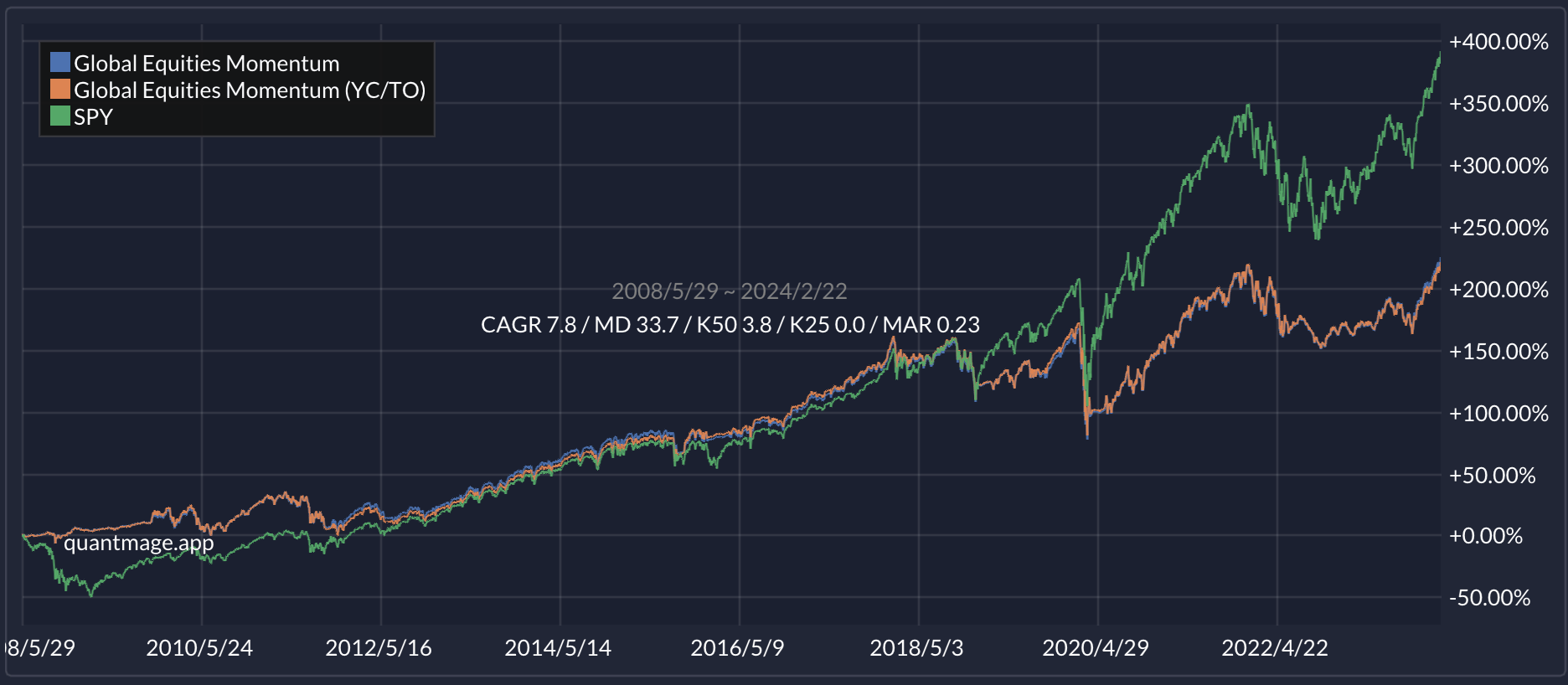

Gary Antonacci didn't stop at theory; he introduced the Global Equities Momentum (GEM) strategy. It's pretty straightforward: compare the 12-month mojo of US equities with something risk-free. If US stocks are rocking, they're then squared off against global stocks (excluding the US) to pick the market leader. If not, it's time to play it safe with bonds or cash. This logic gets a monthly check-up for rebalancing. This video does a great job of explaining it.

In QuantMage terms, this is a breeze to set up. As you can see, it’s using VEU, Vanguard FTSE All World ex US ETF, to represent global stocks.

And the backtest? A cool 7.8% CAGR with a 33.7% max drawdown over 16 years. Compared to just sticking with SPY, it smooths out the ride but might not hit the highest highs.

Taking It Up a Notch with Accelerating Dual Momentum (ADM)

For those feeling a bit more daring, there's Accelerating Dual Momentum (ADM) from EngineeredPortfolio.com. Unlike traditional dual momentum strategies that might use longer-term measures of momentum (e.g., 12-month performance), ADM uses a more responsive approach by measuring momentum across multiple, shorter-term time frames. And SCZ, representing international small-cap equities, is used along with SPY for offensive universe and TLT (iShares 20 Plus Year Treasury Bond ETF) and TIP (iShares TIPS Bond ETF) are used for defensive universe. Monthly rebalancing remains the same.

With QuantMage, implementing ADM is just as straightforward. You can see more responsive 13612W Momentum indicators are used here. It uses 1-month returns to choose between the defensive assets when the going gets tough.

The results? An 11.0% CAGR and a max drawdown of 24.1% over 15 years. It’s worth noting that the slightly shorter period (due to the relatively shorter history of SCZ) allowed it to avoid a potential big drawdown during the Great Recession, though. And the performance drops off to CAGR 7.3% / MD 35.1% when you use threshold trading instead of monthly rebalancing, hinting that timing and a bit of luck might have played roles for the original result.

Wrapping It Up

So, what do you think about GEM and ADM? Even if they're not quite your style, the dual momentum concept itself could be a valuable addition to your investment toolkit. For more insights, check out AllocateSmartly's analysis on ADM. ReSolve Asset Management's take on GEM is also illuminating. It sheds light on the benefit of an ensemble approach, where you diversify across many equally legitimate parameter choices, to mitigate specification risk.

Remember, all this is just food for thought. I'm not here to hand out investment advice but to share some intriguing ideas. Always do your due diligence and maybe chat with a finance pro before making your move. Happy investing!