How to Sidestep Momentum Crashes

Market Volatility Foretelling Momentum Crashes

Let’s face it: momentum crashes are the Achilles’ heel of momentum investing. Plenty of folks have tried to figure out how to predict—and dodge—these crashes. I recently stumbled upon a paper titled “Momentum, Market Volatility, and Reversal” that caught my eye. The main idea? Market volatility can predict momentum crashes, and switching to a reversal strategy when volatility is high might just give you an edge. Naturally, I had to put this theory to the test using QuantMage to see if it holds water.

Below, I’ll apply this concept to some strategies I’ve shared before. We’re focusing on cross-sectional (relative) momentum—not time-series (absolute) momentum—and we’ll consider market volatility high when the VIX is above 30.

Equal Weighting

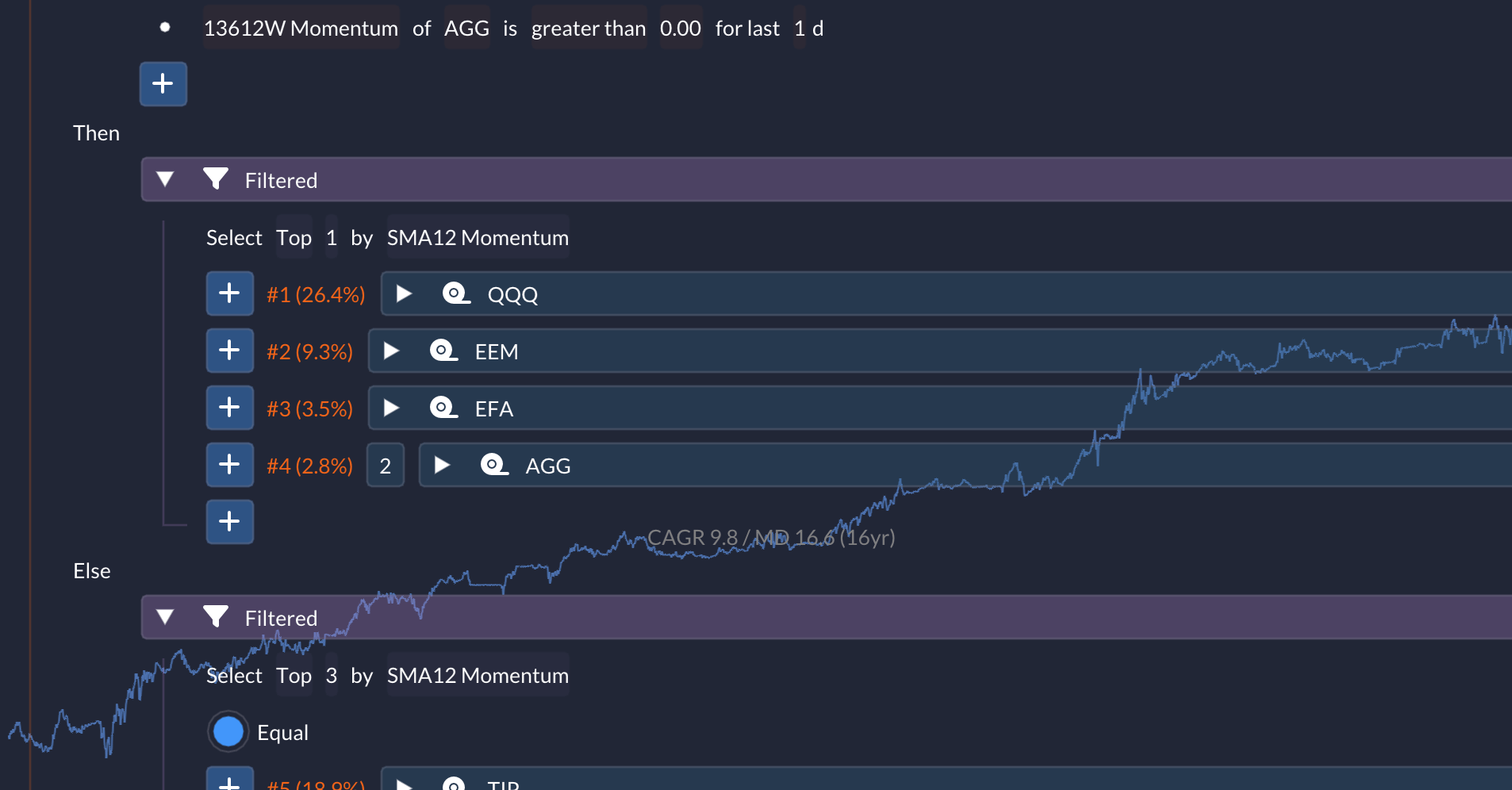

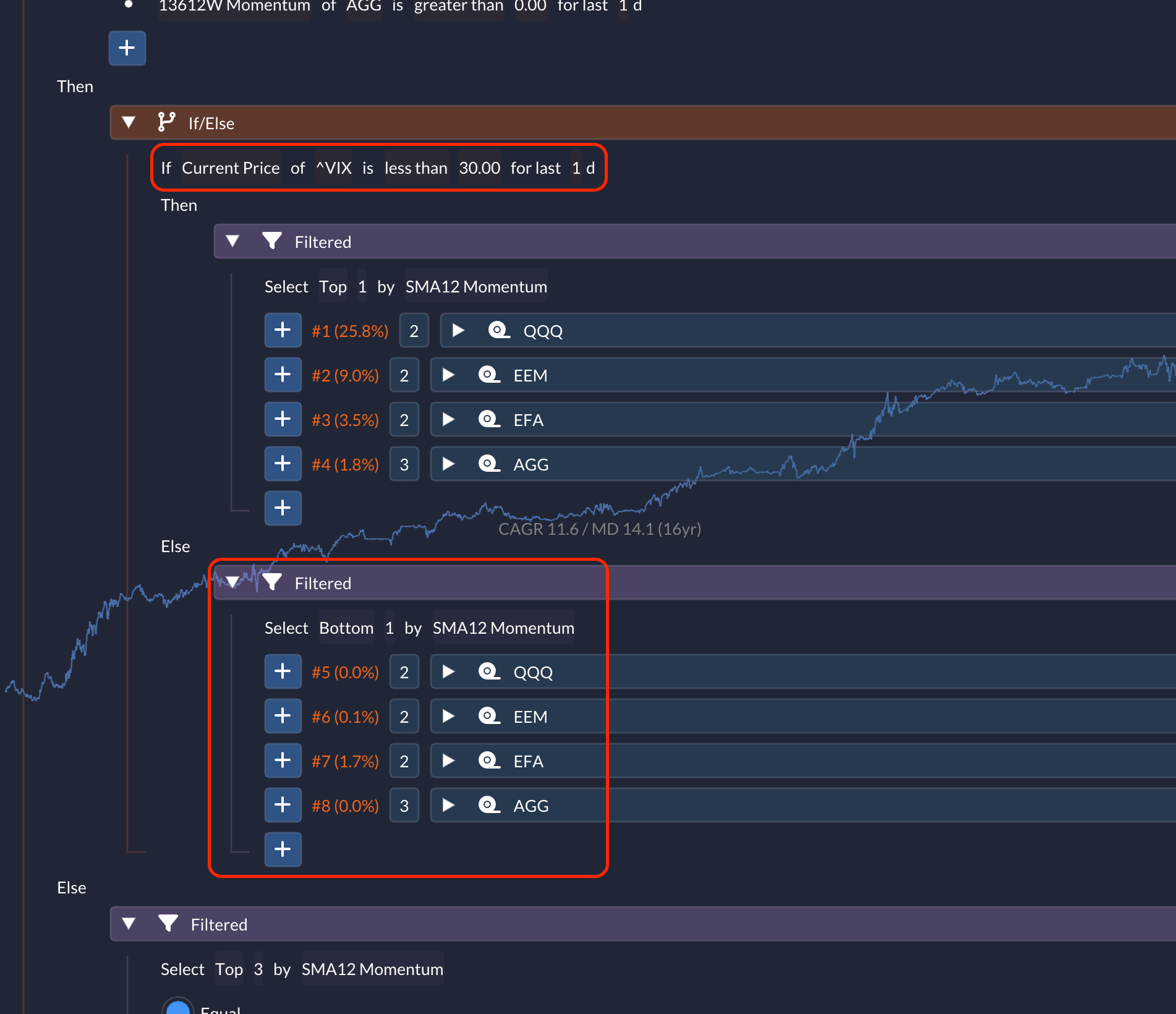

First up, I decided to play it safer when markets get choppy. Instead of piling into high-momentum assets, the idea is to diversify equally across all assets during volatile times. Let’s see how this plays out with the BAA Aggressive strategy. Here’s the original risk-on portion, which uses relative momentum among four assets with a Filtered, along with its performance metrics:

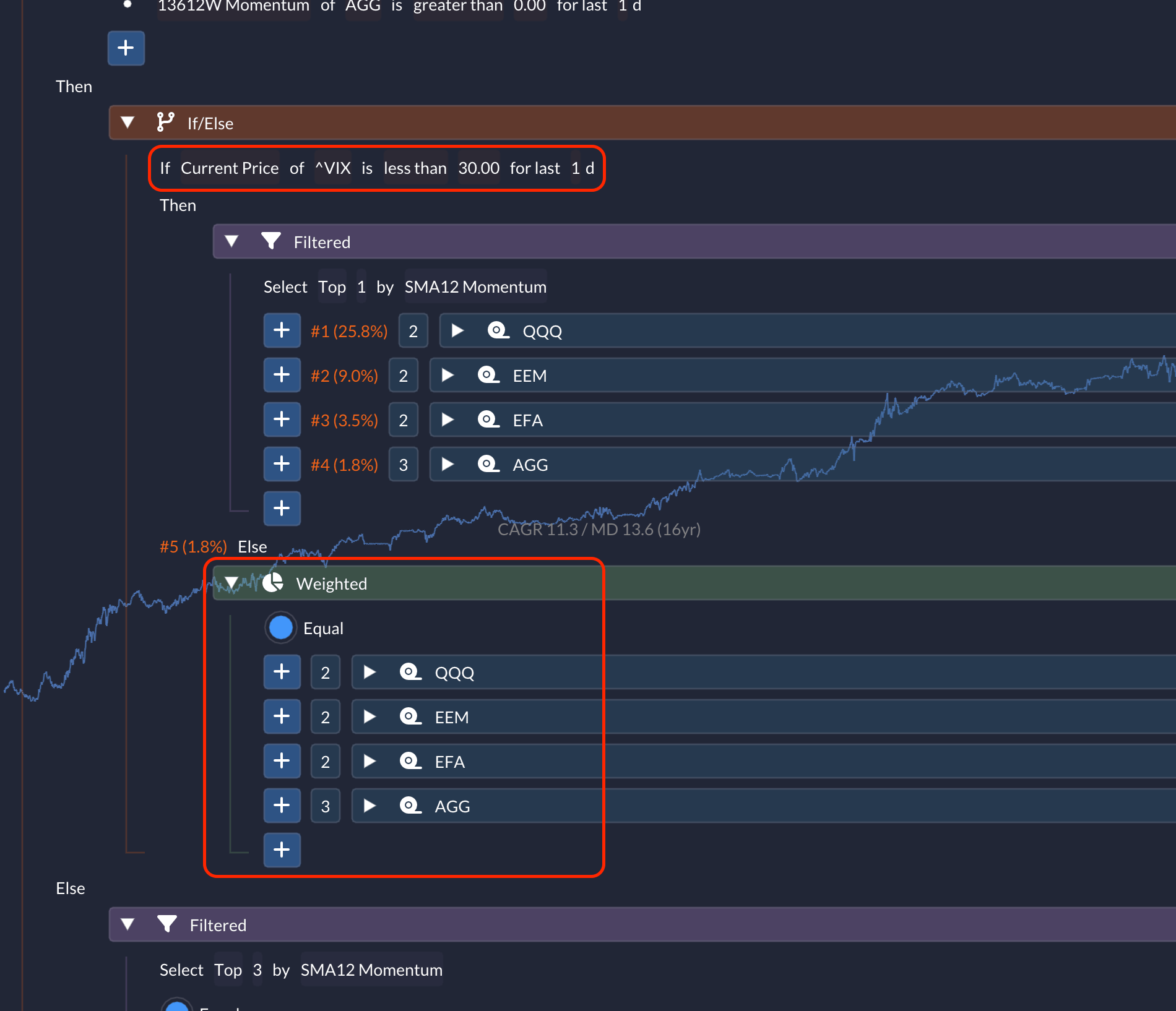

Now, if we wrap it with an If/Else and set up the VIX canary like so, we actually see better performance—a higher CAGR and a lower max drawdown over the same 16-year period:

Feel free to explore the strategy yourself here.

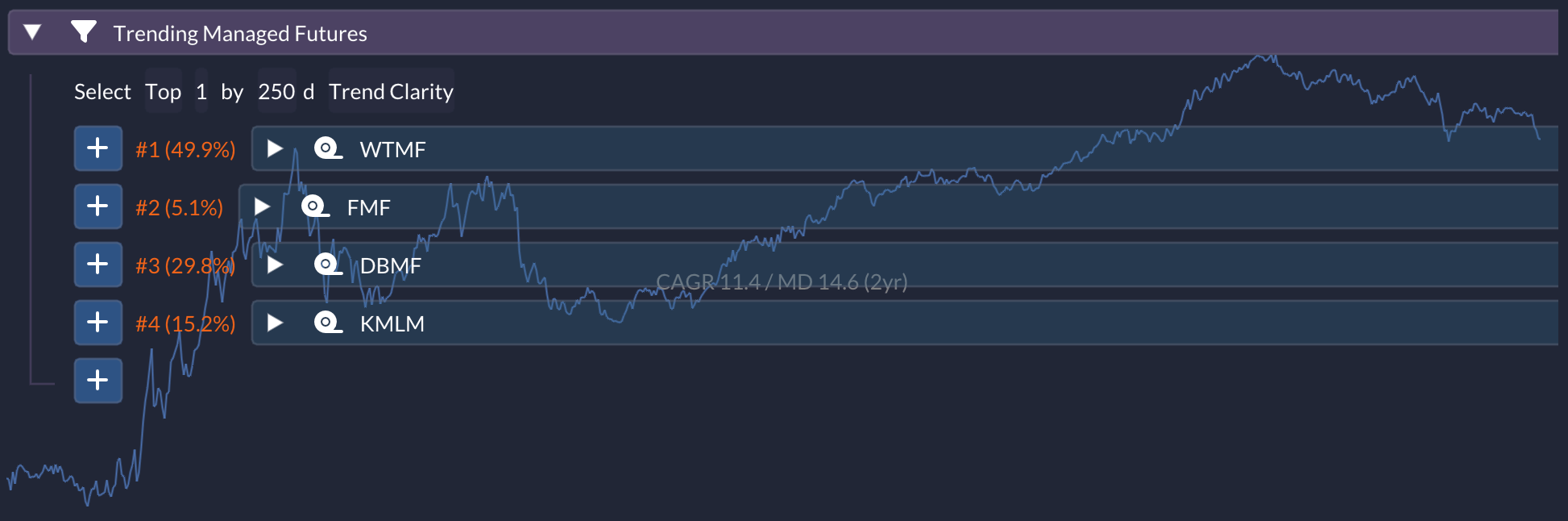

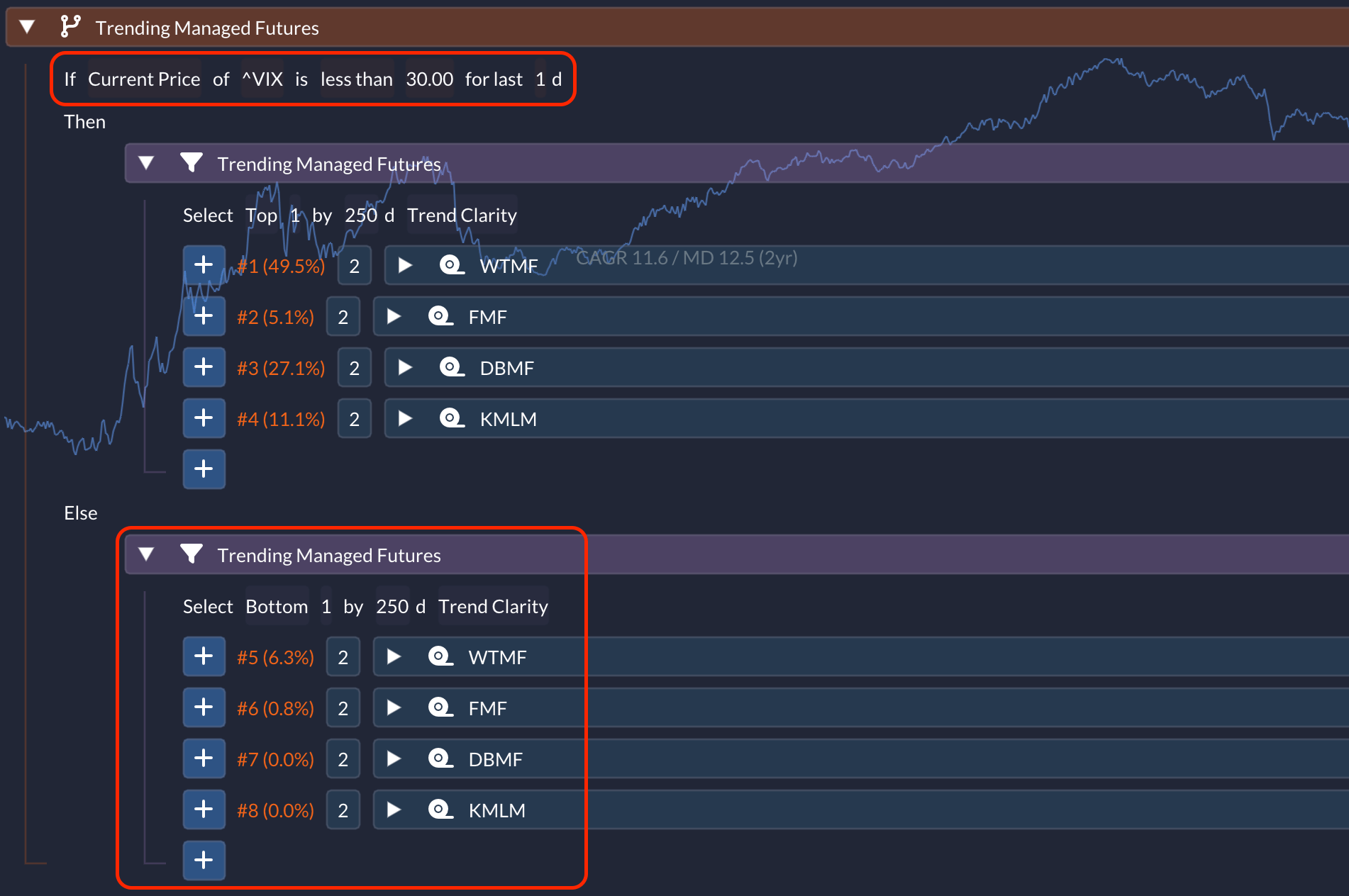

Next, let’s apply the same approach to the Trending Managed Futures strategy. Here’s the original:

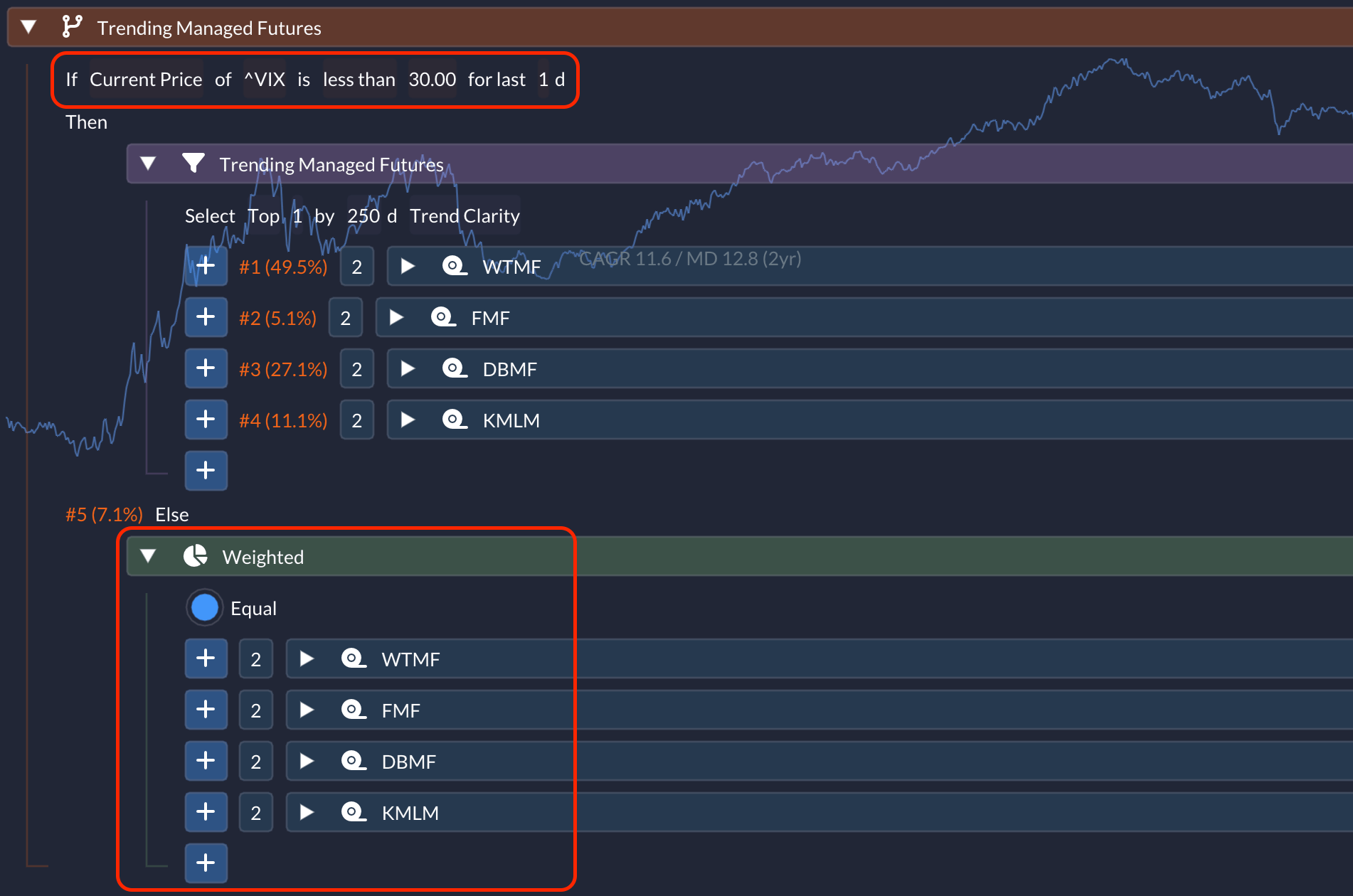

And here’s the revised version:

You’ll notice a slight improvement here as well. But keep in mind, this spell has only a 2-year history, so take the backtest results with a grain of salt.

Mean Reversion

Next up, I wanted to try switching to a mean reversion strategy, as the paper suggests. In QuantMage, it’s as easy as toggling the Filtered’s sorting order from Top to Bottom. Let’s see how this affects the BAA Aggressive strategy:

Once again, we see a comparable improvement. Now let’s check out the Trending Managed Futures:

Another gain here as well!

Short Volatility

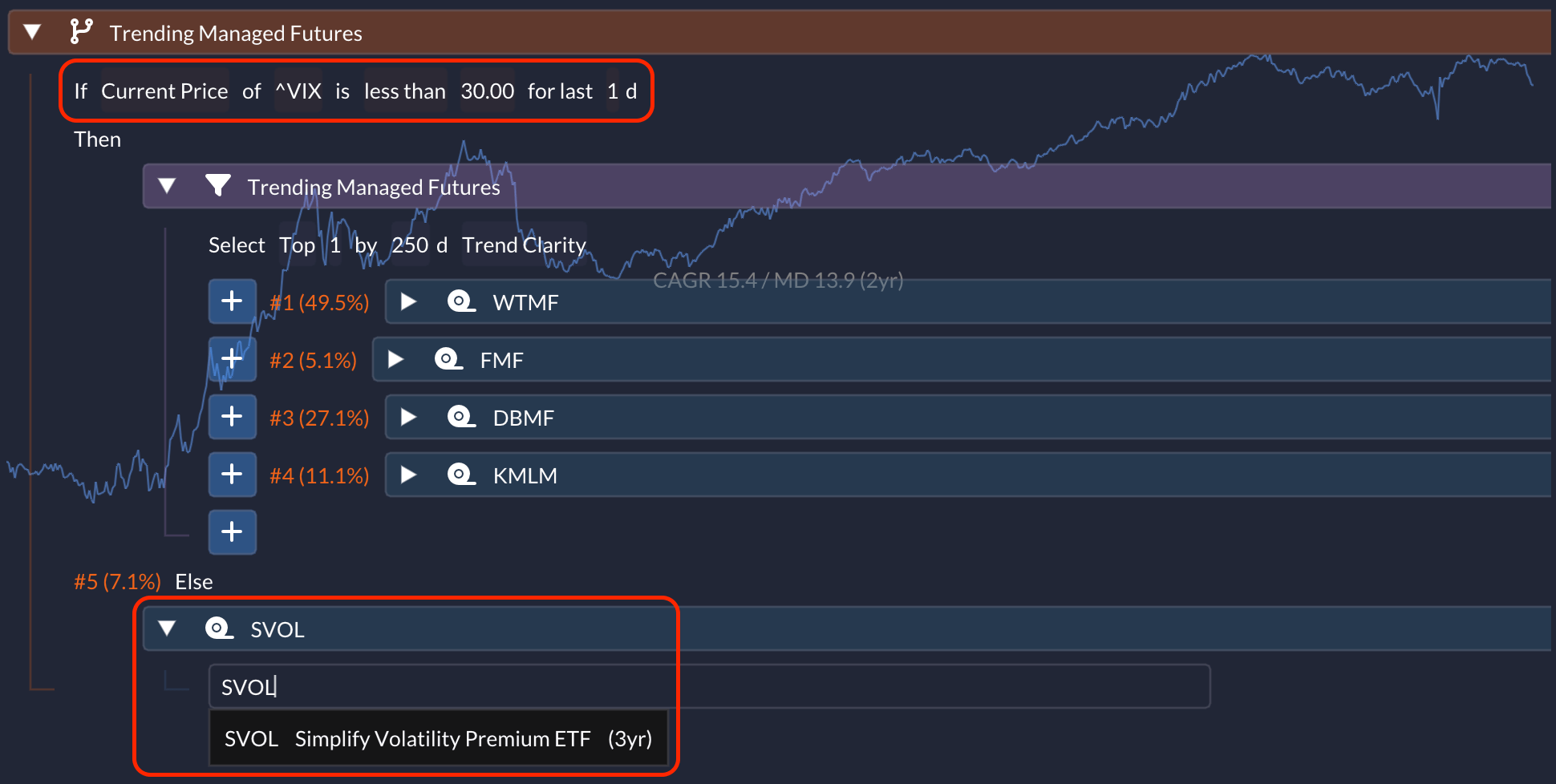

Another idea was to invest in a short volatility asset when the VIX is high, taking advantage of its mean-reverting nature. I used the SVOL ETF for this:

Now we’re looking at an impressive CAGR of 15.4% with a max drawdown of just 13.9%! Again, the 2-year period is pretty short, so don’t put too much stock in it. But feel free to give the spell a whirl here.

📣 Quick note: Everything I share here is purely informational. I’m not your financial advisor, and I’m not telling you to buy or sell anything specific. Always do your homework, and if you’re ever in doubt, talk to a pro.

Bottom Line

These were quick experiments, but they seem to back up the theory. There’s research showing that high-yield spreads can be a great predictor of momentum crashes. Another paper explores how a stock’s proximity to its 52-week high can signal such crashes. This excellent article from Alpha Architect lists a few more references.

So, what do you think? Do you lean more towards momentum or mean reversion? How do you handle the inevitable crashes in your momentum strategies?